$300k Decisions > $30 Decisions

Blog post

09/18/24When trying to build wealth at a faster rate, often the first area people evaluate is their expenses. Maybe this means creating a budget for the first time or cutting ties with unnecessary subscriptions (here are some apps that will help with this). However, while these practices can prove beneficial, their potential upside is limited. Far too often, we see or hear people fixated on cutting costs while much bigger decisions are left unaddressed.

A common example of this is someone who says, “if you stopped purchasing that cup of coffee every morning, that’s $5 every day that you could be investing. This sums to $35 per week / $140 per month / $1,820 per year!” While all that is true, I think it’d be a lot more useful if we looked less at cutting costs – relatively small ones at that – and focused more on ensuring the important topics are addressed. Below are some decisions that will move the needle far more than cutting a $5 expense:

Asset allocation

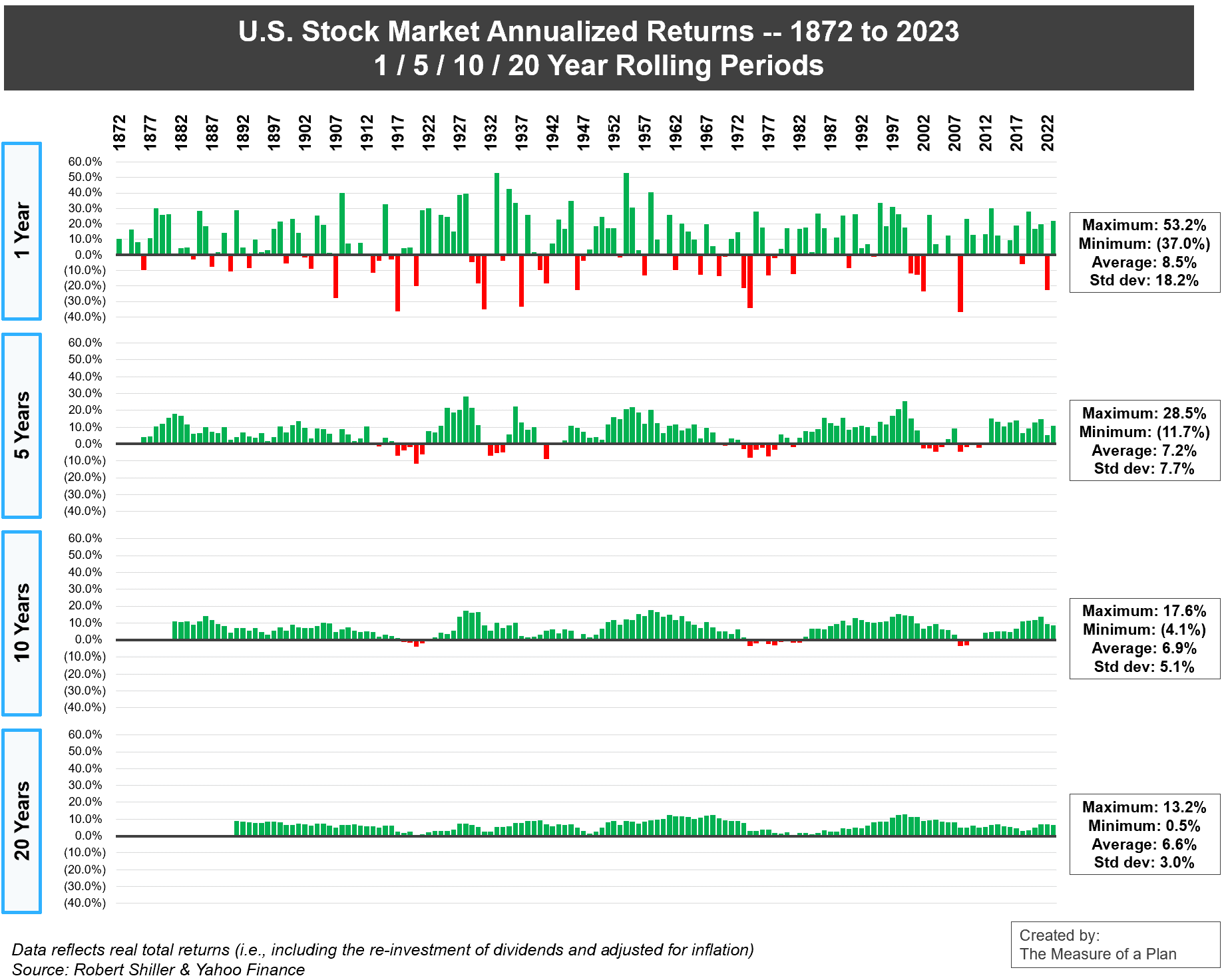

Asset allocation is a fancy term for aligning your investments with your time horizon (when you expect to need the money). The more time you have on your side, the more aggressive you can be in your investments. This is because the market, although it fluctuates up and down every day, has never had a negative return in any rolling 20-year period (see below).

Embedded in this topic about asset allocation is also ensuring you do not have too much money sitting in cash. A large amount of cash that is not invested is guaranteeing that inflation eats away at your purchasing power and is a hindrance to your potential return.

Having an emergency fund

“Wait – I thought that having a large sum of cash on the sidelines means that I am guaranteeing a loss on my money due to inflation?”

That’d be correct. But having an emergency fund actually makes you a better investor. Life will always throw random and unforeseen expenses your way. You want to be able to take these head on and be able to weather them without having to pull money out of your investments. Decide how much you want to always have available between your checking/savings and once it creeps above that threshold, shift the excess to your long-term investments!

Reinvesting dividends

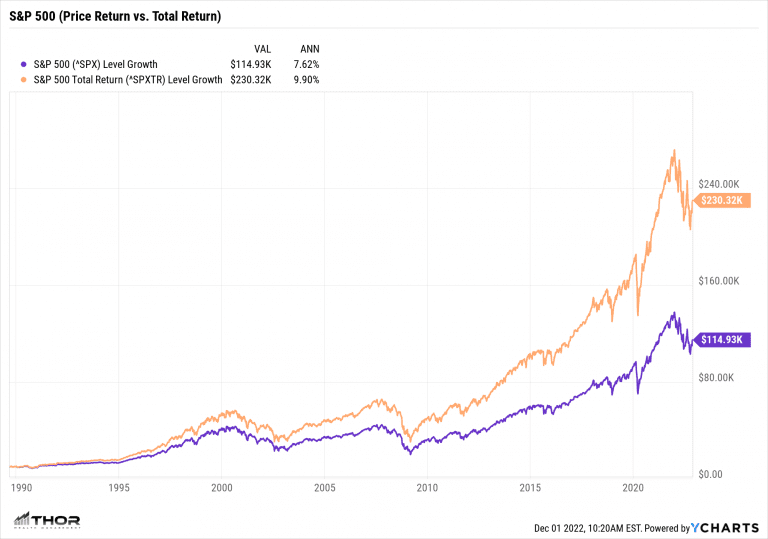

There really is no excuse for this today because almost every financial institution gives you the ability to reinvest dividends with the click of a button. The graph below shows two scenarios where an individual invested $10,000 in the S&P 500 in 1990. The purple line shows you the price return (no dividends reinvested) while the orange line shows you the total return (dividends reinvested).

Saving early

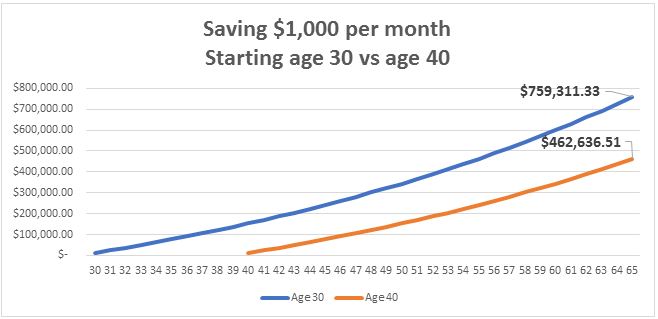

As a surprise to no one, the sooner you can begin saving for retirement the better. The chart below puts this into perspective with actual numbers. It compares someone who starts saving $1,000/month at age 30 versus $1,000/month at age 40. This turns out to be a nearly $300,000 difference age 65.

Warren Buffett is someone who understands compound interest. He began seriously investing at age 10. While many tout his ability to pick winners in the stock market, he attributes his successes to time in the market: “The biggest thing about making money is time. You don’t have to be particularly smart, you just have to be patient”. Very few books or articles about Buffett will highlight the fact that he has been invested in the stock market for over 80 years! At the time of this writing, Buffett’s net worth is ~$144B. But he did not become a billionaire until he was 56. This means that over 99% of his wealth was accumulated after his 56th birthday! It’s hard to wrap our heads around this math of exponential growth vs linear growth.

If you’re asking where you should start saving money to first, here is an older blog discussing the types of accounts to prioritize first.

2-minute Conversations/emails that could save you thousands

Below are some topics that may behoove you far more than cutting out smaller spending habits. Who isn’t a fan of just a little bit of preparation turning into big payoffs?

- Negotiating your salary

- Your income is often your #1 asset. Why not leverage this to utmost of your ability? Receiving an extra percent or two over what was expected can really move the needle for your long-term financial plan. Ramit Sethi talks more in-depth about this in his blog as well as his New York Times Best Selling book, ‘I Will Teach You to Be Rich’.

- Negotiating your rent

- If you are still renting, you should know that landlords are more willing to negotiate than you might expect. Turning over a tenant often means at least one month they won’t be receiving rent. If you are already a good tenant, they will likely be open to hearing you out on your proposal. And again, this is an example of a 2-minute email that could save you thousands of dollars a year.

- Negotiating your credit card limit

- While it may sound extreme to say this is a thousand-dollar move, it can be extremely vital in some instances. 30% of your credit score is determined by your utilization – which is the percentage of your total credit limit that you use. If you increase your credit limit, your utilization rate goes down (which is a positive) and helps boost your score. A higher credit score can mean better interest rates on loans. If you are looking to finance a house, as an example, that can easily equate to thousands saved in interest paid.

Conclusion

While this blog is not an all-encompassing list of what to do to guarantee you are wealthy, the fact remains that there are much bigger things to make sure are addressed before fixating on the little things.

If you have questions and would like to talk with us further, please call us at 513-271-6777. For more THOR reading, click here to go to the Blogs and Market Updates section on our website. Follow us on social media: