Is Leverage Good?

Blog post

06/22/23Leverage is a powerful force that is deeply rooted in our society. It has facilitated the build-out of communities, contributed to the expansion of businesses, and led to countless booms and busts in the economy. While there are many places where leverage has done good, that doesn’t tell the full story.

What Does Leverage Mean?

First, it’s important to understand the different definitions of leverage because they do vary and can cause misconceptions.

According to Merriam-Webster, Leverage is defined as:

Noun:

- : the action of a lever or the mechanical advantage gained by it

- : POWER, EFFECTIVENESS

- : the use of credit to enhance one’s speculative capacity

In many cases people use the term leverage to mean power or effectiveness. Or they think in the context of the mechanical advantage that is gained by using a lever. In these terms, yes leverage is a positive. The misconception comes in the context of financial leverage and because the act of taking on leverage does not always produce good outcomes. Yes, financial leverage can be powerful and effective, but it can also be costly and destructive.

Types of Leverage:

There are many different types of financial leverage but categorizing them into 3 buckets can be helpful.

-

Personal Leverage

Personal leverage is taking on debt to increase your long-term net worth. We recently put out a piece on good debt vs. bad debt. This piece outlines many examples of personal financial leverage and provides a framework to improve decision making.

Commonly you will hear people use the term leverage from a personal perspective. Whether that’s how to leverage your time, your network, or your skills. In these cases, leverage is not the driving force, but a term used to describe power and effectiveness. The force includes things like productivity, scalability, economies of scale, organization, and technology.

-

Business (Corporate) Leverage

Leverage is a core dynamic in business today. It has provided the ability for countless numbers of businesses to get started and others alike to grow to massive heights.

Business or corporate leverage is when businesses borrow funds with the intention of producing greater net income in the future. Businesses can raise capital for many different reasons and this borrowing can appear on the balance sheet in a myriad of different forms. The prudence of this leverage is also a major focus for analysts and investors. The amount of debt on a balance sheet is one measure of that leverage. Analysts will commonly use the amount of debt in comparison to items like EBITDA to diagnose the indebtedness or leverage of a business.

Operating leverage is a different form of leverage in a business. Here you are looking at the amount of fixed cost vs. variable costs. If a company has high operating leverage (high percentage of fixed costs compared to variable), then the business is more affected by a change in revenue.

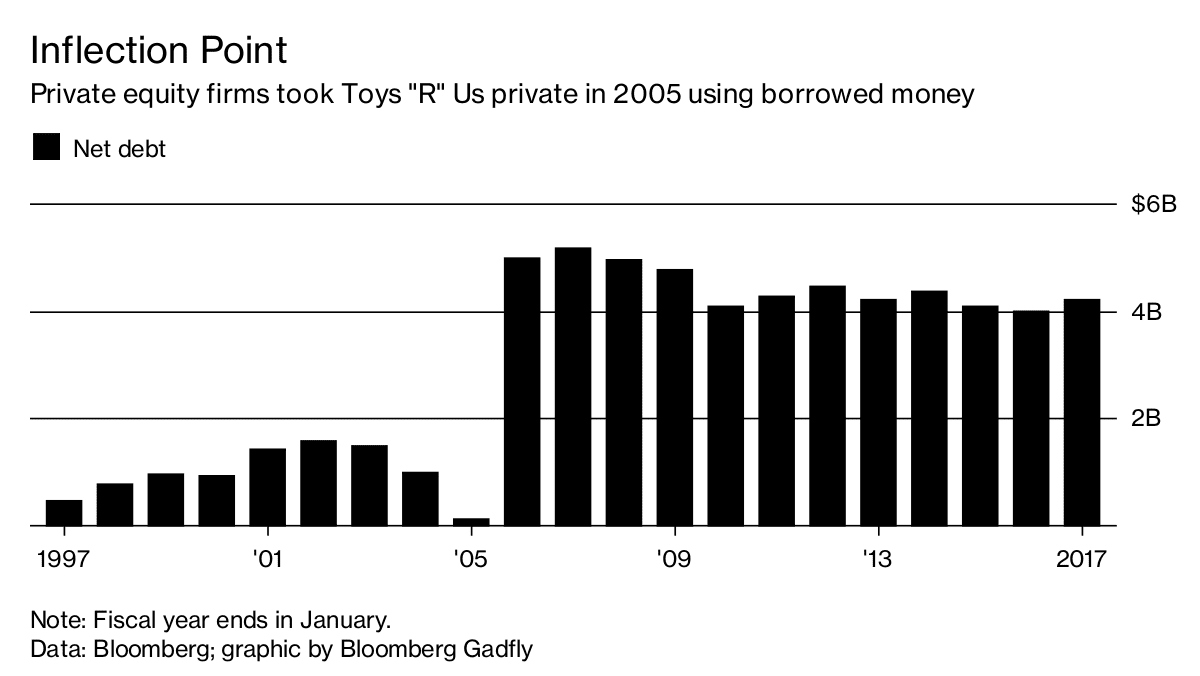

Another context of corporate leverage is looking at sources of funding. Business entities or owners can use the debt markets to borrow funds instead of raising funds via equity. Analysts will look at ratios like debt to equity to understand where a business has raised funds and its amount of leverage. A colorful example of corporate leverage gone awry is the story of Toys “R” Us. Here a leveraged buyout saddled Toys “R” Us, a once thriving business, with so much debt that it was unable to adapt or even survive. Reference the chart below to see the growth in leverage:

-

Investment Leverage

The final type of leverage is investment leverage. Here you can think of leverage at three levels: leverage at the security level, leverage at the portfolio level, and leverage at the system level.

Security Level

Leverage in securities comes in all shapes and sizes. If you buy a publicly listed stock, you are subject to business risk but there is no leverage at the security level. On the other hand, securities such as options and futures have inherent leverage. The nuts and bolts of these securities vary, but they are similar in that you are putting less money to work for the exposure you are receiving. The result amplifies returns, both on the upside and downside.

Another type of security leverage is at the fund level. Commonly people associate hedge fund partnerships with leverage because they are less regulated and speculative in nature, but even mutual funds and ETFs can have leverage.

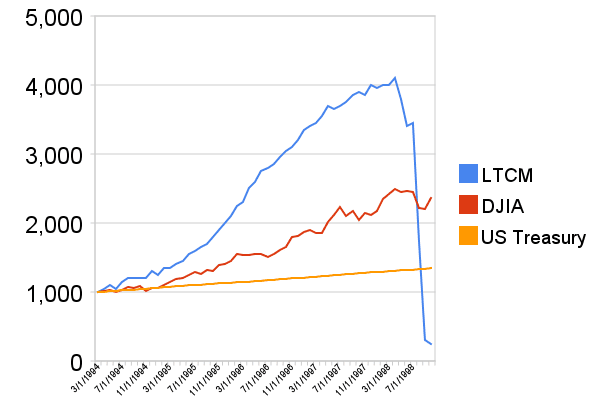

No matter what vehicle you invest in, it’s important to understand how much leverage it will take. A great example of this lesson is the Long-Term Capital Management Crisis. Here you had a hedge fund built by some of the brightest minds in academia and Wall Street. They thought they had a bullet proof system to model risk, so they employed a strategy that took a bunch of small bets and leveraged it to staggering levels. Turns out their model was shortsighted, and they miscalculated the risk. They employed so much leverage that their staggering gains turned to losses that snowballed into eventual ruin. Reference the chart below to see the growth in $1000 invested in Long Term Capital Management compared to the stock and bond markets:

Portfolio

Leverage at the portfolio level is like fund leverage, but here we are not buying the security, we are managing the fund. Take your investment portfolio: If you are buying stocks and bonds with money you have deposited, there is no leverage. Even if you own investment securities like stocks and bonds you can still employ leverage through tools like margin, a pledged asset line, or taking out a loan to invest. Here you also will be able to increase your exposure with less money, but that comes at a cost. The only way to know if leveraging your portfolio is a good idea is if percentage returns are greater than percentage costs on your borrowing, and that is only clear in hindsight.

Systematic

Leverage in the system speaks to the systemic risk of leverage. This is a collection of all the personal, corporate, and investment risk. A good example to highlight systematic leverage is the 2008 financial crisis. This was the perfect storm of leverage: At the personal level people were overextended with multiple mortgages. From a security level there was excessive securitization and creation of complex products. And from a portfolio level investors and banks alike were over invested. To give you some perspective, banks had 23 dollars of deposit liabilities for every dollar they had in liquid cash. The buildup of this much systematic leverage amplified the eventual economic bust and recession.

Conclusion

While we can’t definitively say that financial leverage is good, we also can’t ignore the powerful force that leverage plays in our financial world. We need to be cognizant of the amount and cost of leverage because in financial markets risk and returns are only clear in hindsight.

It’s better to think about leverage as a tool, like we do with diversification. To continue with the tool analogy, diversification is like a screwdriver and leverage is more like a buzz saw. While a saw allows you to construct things you wouldn’t have been able to otherwise, like a bookshelf or a house, it can also be dangerous. If you don’t know how to use the saw or have a healthy respect for the blade, you can cut your finger off.

If you have questions and would like to talk with us further, please call us at 513-271-6777. For more THOR reading, click here to go to the Blogs and Market Updates section on our website.

Follow us on social media: